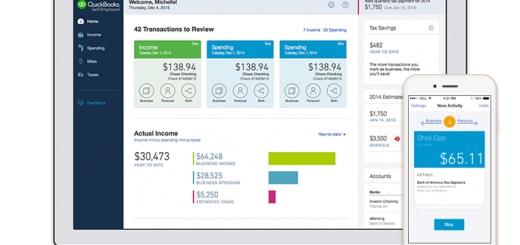

支付服务Stripe与会计税务服务Intuit联手,为小型企业和劳动者更好地追踪自己的财务

创业公司 Stripe 致力于为随“按需经济”兴起的一大批新型服务增强支付功能,这些服务为劳动者提供了各种按需赚钱手段。与此同时,为小型企业和个体经营者开发会计及税务软件的 Intuit 致力于帮助那些劳动者更好地追踪自己的财务状况。

因此,Stripe 和 Intuit 联手开发一款“在按需劳动者收到付款时立刻识别为收入,并帮助他们冲销工作相关费用从而优化税金”的产品也就合情合理了。

通过这一合作产品,在使用 Stripe 支付的按需平台上工作的劳动者将能够方便地连接 Intuit 最新的个体经营者版 QuickBooks 在线软件 。连接完成后,QuickBooks 产品就能立刻将支付款项识别为收入,并由此帮助劳动者追踪自己的财务状况——尤其是在义务纳税方面。

据 Intuit 个体经营者解决方案的副总裁、总经理亚历克斯·克里斯(Alex Chriss)称,大部分 1099 劳动者(译注:即收入为税前收入、年底报税的个体经营者)通常都不知道自己每月、每季或者每年的收入。部分原因在于,与拿工资的员工不同,他们不会收到定期的工资清单——相反地,他们是从所工作的按需平台上收到不定期的支付款项。

另外,他们不善于记录可以用来冲销税额的开支,不过这又是另一个话题了。

为了吸引不断增长的按需劳动者或者 1099 劳动者,Intuit 将个体经营者版 QuickBooks 免费开放。每月 7.99 美元则会获得一些付费功能,比如允许用户在软件中连接银行账户和信用卡,从而追踪收入和支出并予以分类。

Intuit 希望以免费试用的方式,通过 QuickBooks 让劳动者对自己的财务状况有更多的了解。比如说,能够估算出需要缴纳多少的每季税金和年终税金。这就避免了收到巨额税单或者因每季纳税不足而被处罚的可能性。

为了简化收入追踪流程,QuickBooks 中集成 Stripe 的功能将会向从使用 Stripe 作为支付手段的公司获取收入的劳动者免费开放。据 Stripe 战略合作关系主管克里斯蒂娜·科尔多瓦(Cristina Cordova)称,其中包括了 Lyft,Sidecar,Summon,Flywheel,Handy,Homejoy 以及 Washio 这样的公司。

由于这些公司以承包商的形式雇佣劳动者,他们无法提供税务方面的建议或福利。然而通过直接在 QuickBook 这样的产品中追踪收入,那些个体经营劳动者就能够更好地管理自己的财务。

另外值得注意的是,双方的合作只是帮助到了一部分按需劳动者,并不是所有的。比如说 Uber 司机就无法享受这一福利,因为 Uber 并不使用 Stripe。不过这些劳动者仍然可以使用付费版 QuickBooks 连接自己的银行账户。

无论如何,这不正是免费增值商业模式的美妙之处么?

Stripe Partners With Intuit To Help On-Demand Workers Keep Track Of Their Finances

Startup Stripe helps to power payments for a large number of new services offering up ways to make cash as part of the growing “on-demand economy.” Meanwhile Intuit, which makes accounting and tax software for small businesses and the self-employed, wants to help those workers keep better track of their finances.

So it makes sense for Stripe and Intuit to work together on a product that will instantly recognize earnings that on-demand workers receive and help them optimize their taxes with write-offs for work-related expenses.

Through the partnership, people who work for on-demand platforms that make their payments through Stripe will be able to easily connect with Intuit’s new QuickBooks Online Self-Employed software. Once that’s done, the QuickBooks product will be able to immediately recognize payments as income, and as a result will be able to help workers track their finances, and especially their tax obligations.

According to Alex Chriss, who is VP and GM of Intuit’s Self-Employed Solutions, most 1099 workers generally aren’t aware of their monthly, quarterly, or annual income. That’s in part because they don’t get the same income statements as salaried employees — instead they receive irregular payments from the on-demand platforms they work for.

They also aren’t doing a good job of tracking expenses they could deduct from their taxes, but that’s another issue.

To court the growing base of on-demand or 1099 workers, Intuit makes its self-employed QuickBooks software available to use for free. For $7.99 a month it also offers some paid features, like enabling users to connect their bank accounts and credit cards to the software in order to track and categorize income and expenses.

The hope is that by doing so, QuickBooks can provide more visibility into their worker finances. For instance, being able to estimate how much they would need to pay in quarterly and year-end taxes. That can eliminate the possibility of receiving a big surprise tax bill or being hit with fines for not contributing enough in quarterly taxes.

To simplify the process of tracking income, the Stripe integration is being offered for free to workers who receive income from companies that use it for payments. That includes companies like Lyft, Sidecar, Summon, Flywheel, Handy, Homejoy, and Washio, according to Cristina Cordova, who is the head of strategic partnerships at Stripe.

Because those companies hire workers as contractors, they can’t offer tax advice or benefits. But by tracking income directly in a product like QuickBooks, those workers can generally do a better job of managing their finances.

Anyway, it’s worth noting that the Stripe partnership will help some on-demand workers, but not others. Uber drivers, for instance, won’t benefit because Uber doesn’t use Stripe. But those workers will still be able to pay QuickBooks to connect their bank accounts.

Anyway, isn’t that the beauty of the freemium business model?

来源:techcrunch

Dropbox收购设计师协作工具开发商Pixelapse

由 YCombinator 和 StartX 孵化的创业公司 Pixelapse 已经被云存储服务提供商 Dropbox 收购。Pixelapse 已 在博客中宣布了这一消息 ,而 Dropbox 做出了确认。

Pixelapse 提供面向设计师的版本控制和其他协作服务。2013 年,我们 曾将 Pixelapse 比作 GitHub 和 Dropbox 的结合 。(该服务也已 整合了 Dropbox 的功能 。)

该公司表示,“未来一年”,Pixelapse 将继续作为一款独立产品来运营。不过目前看来,最终该服务的用户将逐渐被转移至 Dropbox。

Pixelapse 的创始人这样表示:

我们建立 Pixelapse 的使命在于,为创新人士提供一款版本控制和协作平台。自那时以来,我们很幸运地成为了数十万自由设计师和创新团队日常工作流的一部分。在 Dropbox,开发产品,将这一目标拓展至数百万用户的前景令人非常兴奋。

我们新的开发工作将专注于,当你在 Dropbox 的核心产品之上使用 Pixelapse 时,带来同样的协作和工作流体验。

这笔收购的财务条款并未公布。

Dropbox Acquires Pixelapse, A Startup Building Collaboration Tools For Designers

Pixelapse, a startup incubated by Y Combinator and StartX, has been acquired by cloud storage company Dropbox. The news was announced on the Pixelapse blog, and Dropbox has confirmed it.

Pixelapse offers version control and other collaboration tools for designers. Back in 2013, we compared it to both GitHub and, yep, Dropbox. (It’s also been adding integrations with Dropbox.)

The company says that Pixelapse will continue to operate as a standalone product “for the next year,” but it sounds like the eventual goal is to migrate customers over to Dropbox.

The founders write:

We started Pixelapse with the mission of building the definitive version control and collaboration platform for creatives. Since then, we’ve been fortunate to become a part of the daily workflow of tens of thousands of freelance designers and creative teams. The prospect of developing products at Dropbox that expand this vision to millions of users is tremendously exciting.

Our new development efforts will be focused on bringing the same kinds of collaboration and workflow experiences that you’re used to in Pixelapse over to the core Dropbox product.

The financial terms of the acquisition were not disclosed.

来源:techcrunch

硅谷

2015年01月27日

硅谷

IT教育初创企业Pluralsight以3600万美元价格收购Code School

生命不息,学习不止。在各种在线教育公司层出不穷的今天,去哪里学是个问题。而这类公司要想吸引学习者的注意力,就必须在专业性、内容规模等方面做大做强,大鱼吃小鱼成为必然选择。

因此,IT 在线教育公司Pluralsight的战略目标很明确,就是要通过收购小型公司来完善职业 IT 教育培训完整生态链。今天该公司宣布以 3600 万美元收购另一家提供开发教学视频和实训的初创企业 Code School。

Code School 由 Gregg Pollack 成立于 2011 年,总部位于奥兰多。虽然 Code School 成立只有 3 年多的时间,但是 Pollack 为开发者提供 IT 教育内容的努力已有 8 年历史。现在 Code School 可以为开发者提供 JavaScript、HTML/CSS、Ruby、iOS 以及 Git 等的教学课程、视频以及截屏,有 web 版和移动 app,尤其注重实践培训,在编程经验有限的开发者中很受欢迎。目前其注册用户数已达 100 万,月活跃用户数为 4 万左右。

在去年 8 月获得了1.35亿美元的融资后,Pluralsight 的荷包很鼓。这已经是 Pluralsight 过去 18 个月 Pluralsight 进行的第 6 笔收购(其他 5 笔收购分别为评测平台Smarterer、创意教学 Digital Tutors、在线技术教育网站 PeepCode、开源课程教学网站 TrainSignal、截屏技术供应商 Tekpub)。此前 Pluralsight 提供的总课程数已接近 4000 门,除了面向 IT 专业人士提供教学内容外(月费 29 美元),Pluralsight 还面向企业提供内部培训课程(收取年费)。这次的收购必将进一步加强 Pluralsight 与其他对手如 Lynda、Skillsoft 等进行竞争的实力。根据 CBInsights 的数据,其估值已达 10 亿美元。

[本文参考以下来源:bits.blogs.nytimes.com, wired.com]

硅谷

2015年01月27日

硅谷

社交客户服务公司Sparkcentral完成1200万美元B轮融资

社交客户服务公司 Sparkcentral 已完成 B 轮融资,募集资金 1200 万美元,此轮融资由 Split RockPartners 领投。Sparkcentral 向企业提供一系列工具,帮助他们经由社交渠道对客户提供支持。

在此之前,Sparkcentral 已经募集资金 560 万美元 ,其中包括在 2013 年 10 月份完成的 450 万美元 A 轮融资。鉴于上一轮融资是在 15 个月前完成的,Sparkcentral 的 B 轮融资也处于正常的融资周期内。

我向 Sparkcentral 提了一个问题,即为何决定在 B 轮融资中募集资金 1200 万美元,因为在当前资本环境下,这一融资额只能算适中,即便参照以往的标准衡量。Sparkcentral 首席执行官达维·克斯滕斯(Davy Kestens)对此表示,1200 万美元融资额“符合公司增长曲线,”也是基于 Sparkcentral 在扩充团队规模和功能集时所需要的资金做出的一个决定。

同科技行业其他没有进入“死亡漩涡”(death spiral)的公司一样,Sparkcentral 也正在招募人才。该公司预计 2015 年员工数量将从现在的 30 人增至 60 人。Sparkcentral 的业务目前在美国和比利时两地同时展开。

Sparkcentral 究竟是做什么业务的?为此,我采访了 Sparkcentral 联合创始人马特·芬尼兰(Matt Finneran),他表示 Sparkcentral 曾经是一家专注于客户服务的社交媒体公司,现在则将自己定位于一家专注社交媒体的客户服务公司。在芬尼兰看来,Sparkcentral 不同于社交媒体管理领域的其他公司,比如总部设在芝加哥的 SproutSocial,因为它的业务重点并不在市场营销方面。

我本希望 Sparkcentral 能提供一下详细的最新财务数据,但该公司只是给出了比较数据,而非绝对数据。这样一来,我们只能对 Sparkcentral 最近的财务状况有个大概的了解。据 Sparkcentral 介绍,该公司 2014 年营收比 2013 年增长 320%。同期,Sparkcentral 客户数量增长了 100%。这两项数据表明,Sparkcentral 的客户数量日渐增多,而当前客户的合同价值也不断增长。

我又提到了有关财务的话题,让 Sparkcentral 谈一谈它如何实现增长和开支的平衡—— Box 对未来的收入增长进行了大规模投资 ,而不是将如何扭转短期亏损放在第一位,这种策略曾在 公开市场引发疑虑 。克斯滕斯表示,重要的是拥有“增长路线图”,但不从“悬崖上猛地掉下来”同样关键。

Sparkcentral 之所以不同于其他软件即服务(SaaS)公司,原因是由于有些客户属于 Delta 这样的大公司,月度经常性收入(MRR)与年度经常性收入(ARR)之比可能超出了正常标准范围——换句话说,我估计 Delta 不是按月向 Sparkcentral 支付购买软件的费用。克斯滕斯表示,鉴于此,该公司在追踪自家财务表现时更注重季度数据,也就不足为奇了。

在一个拥挤但增长迅速的科技细分市场,Sparkcentral 取得了飞速发展。该公司拥有实现发展计划所需要的资金,现在的问题是这些计划能否得到执行。我会在未来几个季度继续关注这家公司,看一看能否弄到最新的营收数据。

Social Customer Service Firm Sparkcentral Locks Up A $12M Series B

Sparkcentral, a company that provides tools to help businesses conduct customer support over social channels, has raised a $12 million Series B round of funding, led by Split Rock Partners.

The company previously raised a total of $5.6 million, including a $4.5 million Series A round of capital in October of 2013, or around 15 months ago. That places the company’s Series B round inside of a normal raising schedule.

I asked Sparkcentral why it decided to raise $12 million for its Series B — in the current capital climate, the sum is slightly modest, even if standard by historical norms. The company’s CEO Davy Kestens indicated that the sum “fit [the company’s] growth curve,” and was predicated on how much money Sparkcentral would need to expand both its staff, and feature set.

Like quite literally every company in technology that isn’t entering some sort of deathspiral, Sparkcentral is hiring. The firm, which splits its operation between the United States and Belgium, expects to double its current 30 person employee base in 2015.

So, what is Sparkcentral? I spoke to its co-founder Matt Finneran, who indicated that the company was once a social media company focusing on customer service, but now thinks of itself as a customer service firm that focuses on social media. In the view of Finneran, Sparkcentral is different from other players in the social media management space because it does not have a marketing focus, like the Chicago-based Sprout Social.

I asked the company to detail is recent financial performance, and it responded with comparative, and not absolute data. That weakens the dataset. Still, according to Sparkcentral, its revenue grew 320 percent in 2014, when compared to the year prior. During that same period, its customer based expanded 100 percent. Those two figures imply that the company is landing increasingly large clients, that it is seeing increasing contract value among current customers, or some combination of the two.

Continuing the financial theme, I asked the company how it weighed a balance between growth, and spend — Box famously invested heavily in future revenues, only to see its short-term losses spook the public markets. Kestens indicated that it is important to have a “roadmap for growth,” but that it is also critical to not “drive off a cliff” at full clip.

Sparkcentral is different from other SaaS companies in that, given that some of its clients are large firms like Delta, its ratio of monthly recurring revenue to annual recurring revenue (MRR v. ARR) is likely outside of the norms — I presume that Delta isn’t paying for much software on a monthly basis, in other words. Kestens said that his firm is, given that, unsurprisingly more focused on quarterly data when it comes to tracking its own performance.

SparkCentral has grown quickly inside of an expanding, if crowded technology market category. It has the capital to pull off its plans, so now the question is execution. I’ll check in with the firm in a few quarters, and see if I can scare up some new revenue numbers.

IMAGE BY FLICKR USER DANIEL DIONNE. UNDER CC BY 2.0 LICENSE (IMAGE HAS BEEN CROPPED)

来源:techcrunch

硅谷

硅谷

硅谷

硅谷

硅谷

硅谷

硅谷

硅谷

硅谷

硅谷

硅谷

硅谷

硅谷

硅谷

硅谷

硅谷

硅谷

硅谷

扫一扫 加微信

hrtechchina

扫一扫 加微信

hrtechchina